-

2016-06-22

Background

Today E-commerce is a constantly developing business. New Technologies assist global business to be operated without permanent establishment (PE) in Country of source (COS). Today traditional businesses conduct their business with new technologies. And completely new businesses are developing.

Under the existing legislation, COS can tax a non-resident providing E-commerce services only if the non-resident has a PE in the COS. And a PE is defined as a ‘fixed place of business’ which excludes E - commerce. Therefore, E-commerce companies do not need PE in any COS. They can set up the companies in tax havens and avoid Country of Residence (COR) tax also apart from COS tax.

Committee on taxation on E- Commerce (formed by the CBDT) took cognizance of the Report on Action 1 of Base Erosion & Profit Shifting (BEPS) Project. The BEPS Report on Action 1 clearly highlights the need for modifying existing international taxation rules, and identifies three options-

i) A new nexus based on significant economic presence,

ii) A withholding tax on digital transactions, and

iii) Equalization Levy (EL).

After examining the three options identified in the report, the Committee notes that compared to the first two options (which would require changes in a number of tax treaties), the third option of ‘EL’ provides a simpler option that can be adopted under domestic laws without needing amendment of a large number of tax treaties.

Based on the report of the Committee, Chapter VIII namely “Equalisation Levy” has been inserted in Finance Act, 2016 to tax specified services. - Applicable date is 1st June,2016.

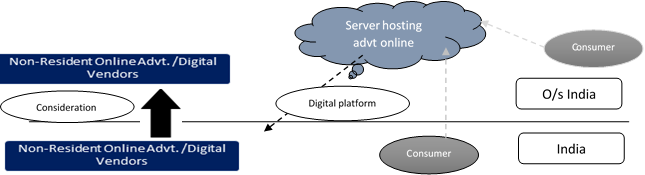

EL - Applicability?

Tax status till 31st May, 2016:

i) No tax withheld on payment for online Advertisement/ use of Digital platform for advertising Indian products/ services.

ii) NR Vendors has server in low tax jurisdiction and has no PE (Permanent Establishment) in India but has significant presence through digital platform in India.

iii) No income is being offered by Non-resident offering online advertisement / digital platform in India.

EL- Key Aspects

1)EL is to be charged only on non-residents of India.

- Indian E-commerce companies like Flipkart, Snap Deal etc. are not liable to EL.

2) EL @ 6% on ‘specified services’ for consideration exceeding INR 1 Lakh during the year.

- Onus on payer irrespective of payee disagreeing for such levy from his payout.

- ‘Payer’ need to be carrying business in India.

3) ‘Specified services’ defined to currently include payments made to non-resident vendors1 towards the following:

- Online2 advertisement

- Provision for digital advertising space

- Any facility or service for the purpose of online advertisement

4) Payment for ‘non-specified’ services out of ambit of EL.

- Payment for computer software license, AMC services, Journal/Newsletter subscription, Royalty, Technical service Fees not subject to EL.

- No EL on goods sold through E-commerce. Therefore, Customer buying goods on “Alibaba” not subject to EL.

5) Introduced as a separate chapter under the Finance Act

- The levy is not under the Income-tax, Act, 1961 but borrows certain provisions from it.

- Such charge / levy not in the nature of ‘income tax’ hence Tax Treaty benefits not available.

- It is an additional charge on Indian payer.

6) Income in hands of non-resident recipient exempt from ‘income-tax’, if transaction charged to EL.

- EL and income-tax cannot be levied simultaneously. They are mutually exclusive.

7) EL and Service Tax are two difference levy and governed by two separate Acts.

- One need to assess applicability of service tax on import of advertising services as per Finance Act, 1994 as amended from time to time as well as related rules.

EL- Challenges ahead:

1) Whether Equalisation Levy applicable on-

- Outstanding payables as on notified date?

- Advance payments made whereas invoices raised subsequent to notified date?

2) Whether EL to be grossed up or to be applied on net amount?

For e.g. : If Payment for online Advertisement is Rs. 500,000, then 6% EL computes to Rs. 30,000. However, if grossing up concept is applied then, EL computes to (Rs.500,000/ 94%* 6%) Rs. 31,915 and amount will be borne by the recipient of the service.

3) Is the present online payment system geared up to permit ‘deduction’ of levy on payment or ‘grossing up’ is the only recourse?

- Further, will grossing up shield the payer from penal consequences?

4) Should such transactions pass through form 15CA and 15CB certification?

5) No provision for assessment or appeal against intimations issued by tax authorities.

EL- Compliance Cycle steps

1) Deduction of EL from amounts paid/ payable

2) Deposit of EL by 7th of the following month

3) Filing of annual statement - Due date/ forms to be prescribed

4) Issue of intimations by tax authorities

5) Filing of rectification applications

Implications in case of non-compliance

1) Non-deduction/ non-payment of EL could lead to the following-

- Disallowance of expenditure

- Interest at 1% pm for delay in deposit of EL + Penalty3 leviable upto 100% of the EL amount

2) With respect to filing of annual statement

- In case of non-filing –Penalty4 of Rs 100 per day of default

- Imprisonment upto 3 years in case of any false statement made in annual statement.

EL applicability Illustrations:

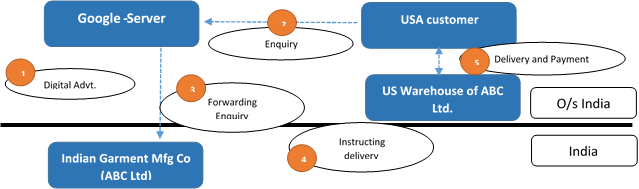

Case study - 1:

Analysis:

- Consideration paid to Google for Advertising subject to EL.

- But, had this charges been incurred by US Agent/ subsidiary of ABC Ltd. out of Sales Commission received from ABC Ltd., it would have been out of ambit of EL.

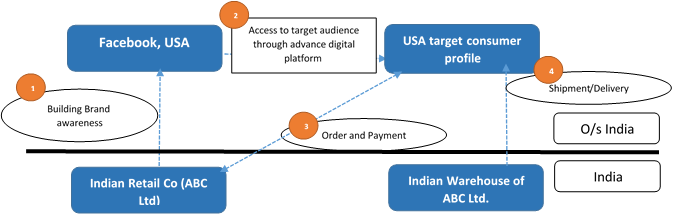

Case study - 2:

Analysis:

- Fees paid to Facebook for brand awareness campaign would attract EL. EL would be attracted even if no single consumer had approached ABC Ltd.

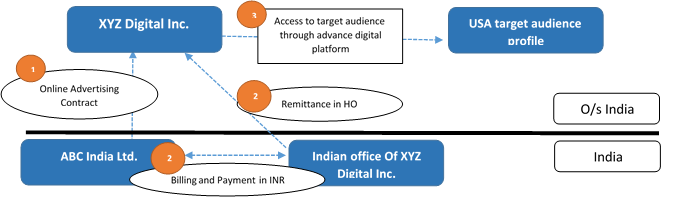

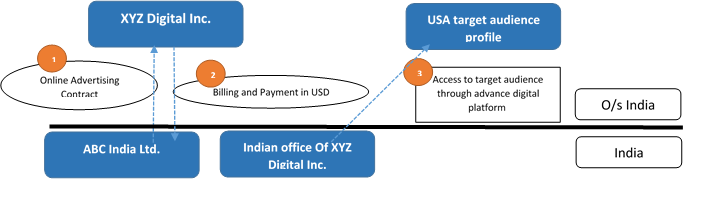

Case study - 3:

Analysis:

Analysis:

- Apparently, Fees paid to Indian office of XYZ Digital Inc. towards advertising and marketing campaign may attract EL, as charging provision of EL apply for payment made to Non-resident irrespective of fact where he receives. Further clarity awaited on EL application in such case.

- However, in such case, if for time being, EL is applied, such payment would not attract Income tax in India on ‘Receipt’ basis in hands of XYZ Digital Inc. As per interpretation of EL provisions, Government may have to forgo higher tax collection, which they are entitled in current system5

Case study - 4:

Analysis:

Payment made to XYZ Digital Inc in US currency towards online advertisement will not attract EL as service is ‘effectively’ rendered by Indian office of XYZ Digital Inc. (PE in India) and transaction is effectively connected with that PE and income from the transaction will be taxed in India @40% plus surcharge and Education cess. Further, in this scenario, withholding tax implication under section 195 need to be examined.

1 not having a permanent establishment in India

2 ‘Online’ means a facility/ service/ right/ benefit or access obtained through the internet or any other form of digital or telecommunication network.

3 Provisions for assessments and appeals only in respect of penalty.

4 Provisions for assessments and appeals only in respect of penalty.

5 It is assumed that such receipt is also taxable as per provision of DTAA with respective country.